Why Choose Credaegis?

Knowledge is Power. Especially When It Comes to Your Money.

Welcome to Credaegis Shiksha, our promise to you. In a world of confusing terms, hidden fees, and tempting offers, we believe your best defence is knowledge. This is not just a guide; it's an education. Here, we will question the "easy" options, uncover the hidden traps, and empower you to become the master of your financial destiny. Let's begin this journey to financial freedom, together.

What is This "CIBIL Score" and Why Should You Care?

Have you ever been told your "CIBIL is low"? What does that even mean? Think of your Credit Score (often called CIBIL score in India) as your financial report card. It's a 3-digit number, usually between 300 and 900, that tells lenders how reliable you are with money. It’s not just a number; it’s your reputation.

A good score (typically 750+) means banks see you as a trustworthy customer. It’s the difference between getting that home loan or being rejected. A higher score also gets you a lower interest rate, potentially saving you lakhs. It affects everything from getting a premium credit card to, in some cases, even post-paid mobile plans.

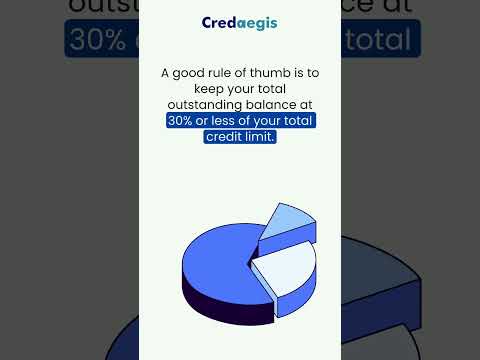

Common traps that ruin your score include paying just the minimum due, applying for too many loans at once (enquiry spree), and missing even a "small" EMI, which stays on your report for years as a black mark.

Your score is your financial story. Are you telling a good one?

That "Loan in 2 Minutes" Ad: Is It a Lifeline or a Financial Ambush?

Your phone buzzes. An app offers you a ₹1 Lakh "pre-approved" loan, credited in minutes. It feels like a blessing during a tough time. But is it?

They deduct a "Processing Fee" upfront, so you get less than you applied for. The interest rate might look like a small number like 2% per month, but that's a shocking 24% per year! For that ₹1 Lakh loan, you could end up repaying over ₹1,26,000.

These loans are designed for the lender's profit, not your well-being. Before you click "Accept," ask yourself: Is this convenience worth the crippling cost?

Quick Video Insights

Watch our short, informative reels for quick tips and clear explanations on important financial topics.

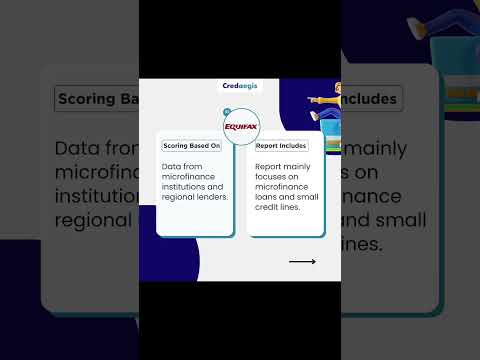

Small Loans, Big Problems: The Unseen Reality of the Microfinance Trap

Microfinance was started with a noble idea: to give small loans to those in rural India who couldn't access big banks. While it has helped many, a darker reality has also emerged: the microfinance trap.

This happens when a person gets trapped in a cycle of debt by taking multiple small loans, often to pay off old ones. This can be due to over-lending by multiple institutions and high-pressure recovery tactics that cause immense distress.

The goal of a loan should be to lift you up, not to push you into a corner. Is the loan serving you, or are you serving the loan?

Borrow with Wisdom. Repay with Dignity.

Think of these as the fundamental rules of borrowing. Your financial "dharma" that protects you.

DO (Your Duties)

✅ Ask "Why?": Borrow for needs (like education, health) not wants (a fancier phone).

✅ Compare Lenders: Check offers from at least 3-4 different banks/apps. Don't marry the first offer.

✅ Read Everything: The fine print is where the traps are hidden. Know the penalties.

✅ Plan Your Repayment: Know the exact EMI and ensure it fits comfortably in your budget.

DON'T (The Traps to Avoid)

❌ Borrow Under Pressure: Never take a loan because an agent is calling you ten times a day.

❌ Sign Blank Documents: This is a huge red flag. Never sign an incomplete form.

❌ Ignore Your Gut Feeling: If a lender seems shady or their methods feel wrong, walk away.

❌ Guarantee a Loan Casually: Becoming a guarantor is the same as taking the loan yourself if they fail to pay.